[read time: 3 minutes]

In my previous entry, I talked about how I’d rather spend four years and five months paying a moderately aggressive amount while enjoying life than two years and ten months paying a very aggressive amount while feeling miserable.

Curious how I came up with those timelines? Let me tell you how we built our payoff plan—estimating we’ll be debt-free by August 2029, almost six years earlier than our loan provider’s estimate of January 2035!

The not-so-secret tool is the Debt Payoff Calculator. This online, web-based tool lets you input your loans or debts by providing the remaining balance, monthly (or minimum) payment, and interest rate.

Using a debt avalanche strategy, it generates a payoff plan that you can then adjust to meet your desired goal. I’ll walk you through how my husband and I set ours up and fine-tuned our plan.

1. Gather Your Loan Information

The first step in setting up the Debt Payoff Calculator is to collect the necessary details for each loan or debt: remaining balance, minimum monthly payment,and interest rate.

As you can see, my loan is actually broken into eight separate loans, plus my husband’s loan. We also recently paid off a personal loan to my parents for our wedding in August 2024, which is why you’ll notice the blank Line 1 in our table.

2. Set Up the Initial Calculation

Once all the information is entered, you can hit calculate—but don’t forget to check the final yes/no question. Selecting “yes” means your payments will remain fixed until all debts are paid off.

In other words, once you pay off one loan, the amount you were paying is automatically redirected to the next highest-interest loan. This keeps your payment amount the same each month while speeding up your debt payoff.

The initial calculation only accounts for making minimum payments. Based on our minimum payments of $1,769.10/month, our loans would be paid off in around 10 years—which is the standard repayment period.

Struggling to make the minimum payments? Call your loan provider! There are usually options available, such as deferment, forbearance, or income-driven repayment plans.

3. Customize Your Payoff Plan

In my previous blog, Crunching the Numbers: A Typical Month, I mentioned that after expenses, we had ~$1,900/month available for either extra loan payments or savings. To create a realistic payoff plan, we explored multiple options:

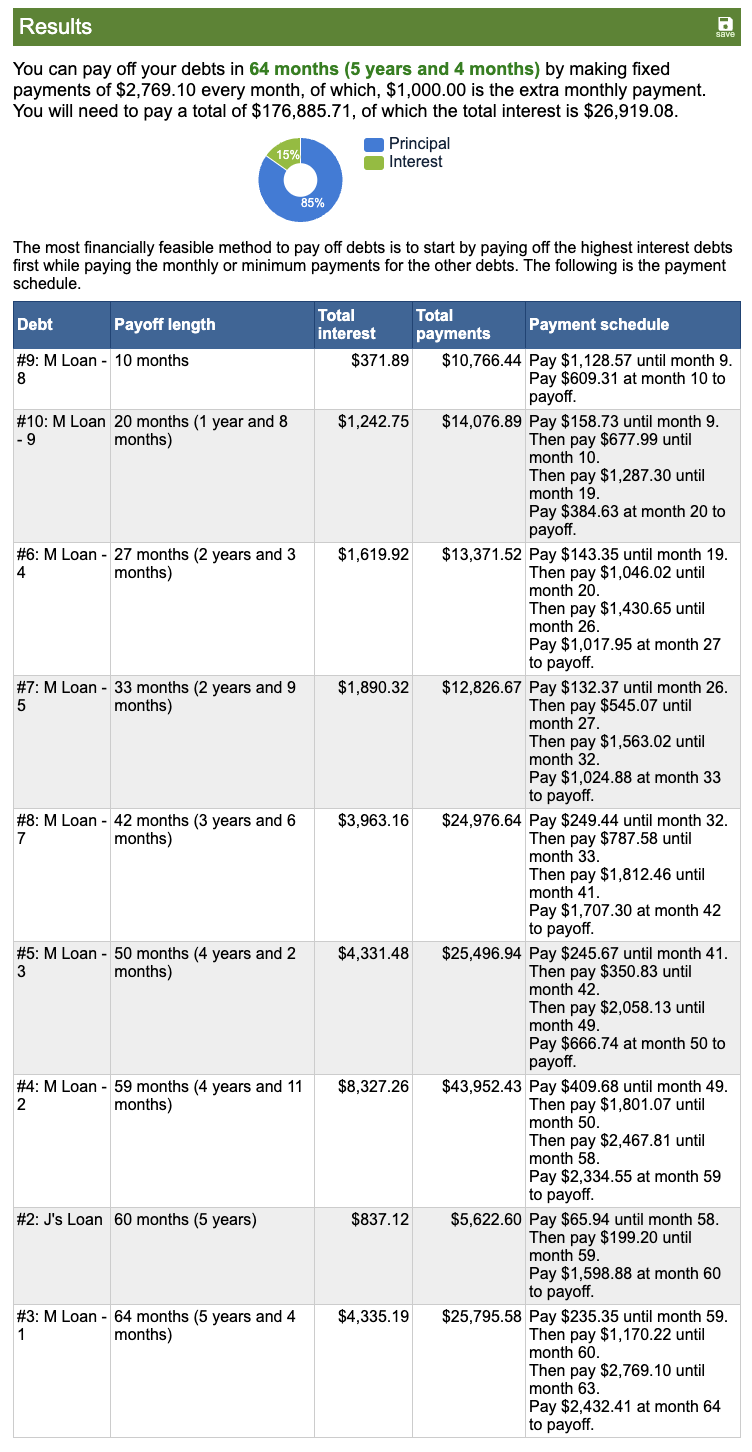

- $1,000/month extra → Debt-free by July 2030 (64 months)

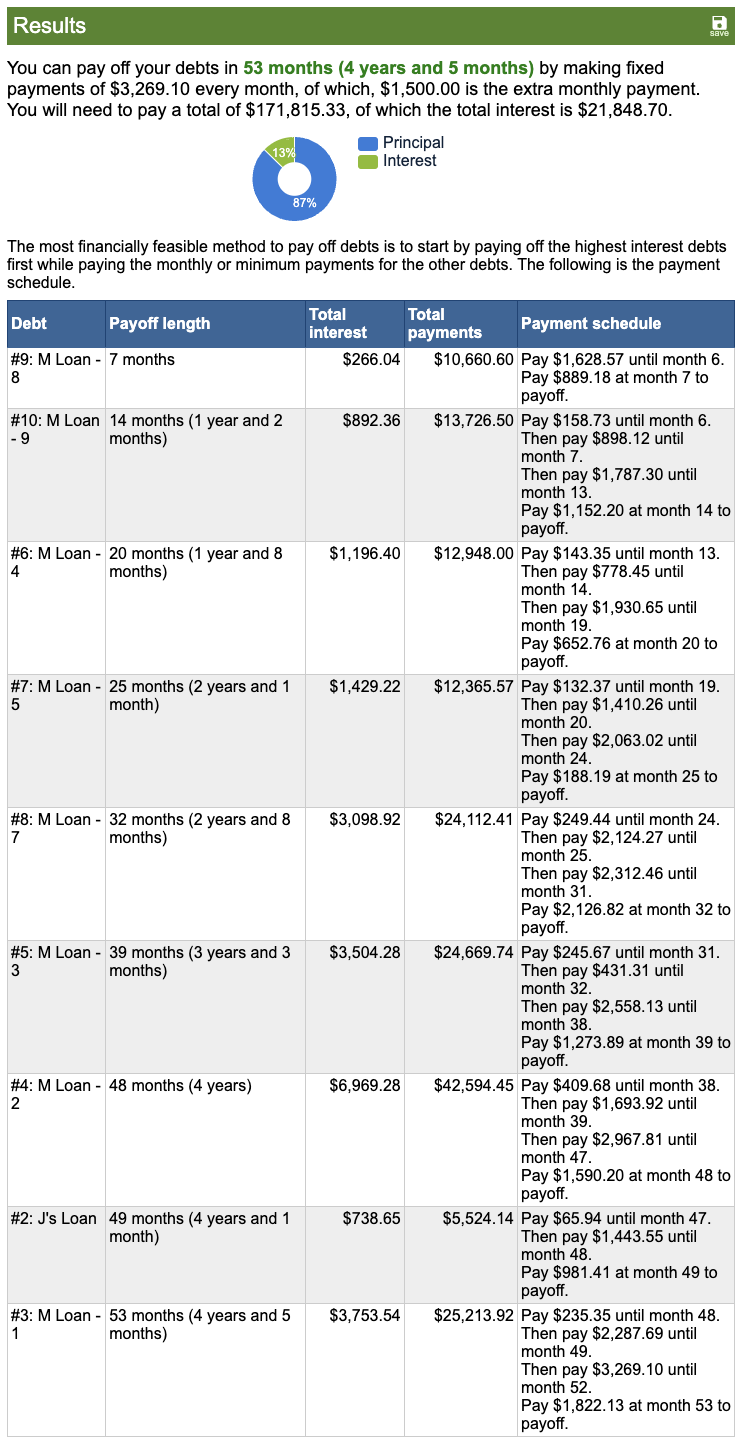

- $1,500/month extra → Debt-free by August 2029 (53 months)

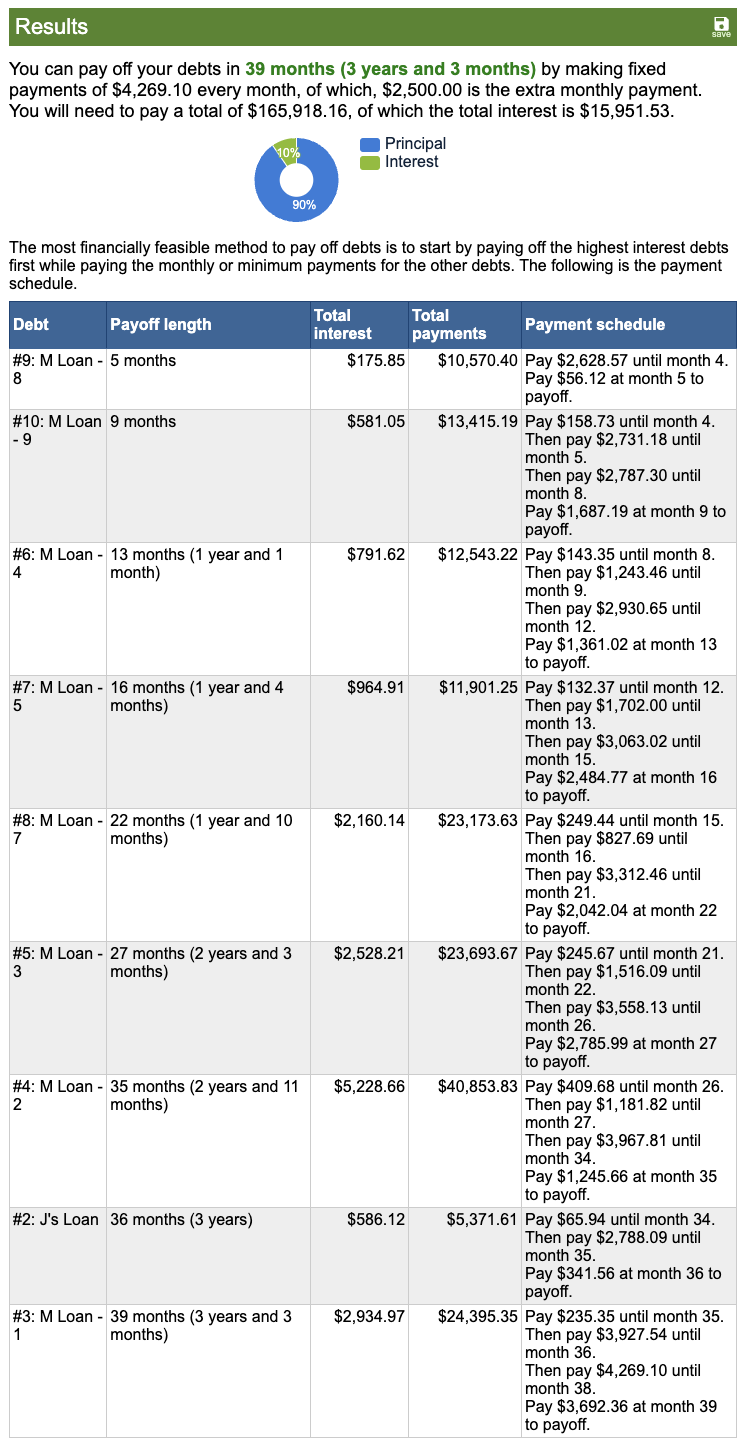

- $2,500/month extra (w/ the potential promotion) → Debt-free by June 2028 (39 months!)

4. Save Your Plan

After discussing our options, my husband and I decided to start with $1,500/month extra payments and adjust as needed. Using the Debt Payoff Calculator, I transferred the plan into a spreadsheet that tracks our monthly goals and shows exactly when each loan will be paid off.

If you are not a spreadsheet person – the Debt Payoff Calculator allows you to save your plan. Simply create a free account and click save in the top right corner, it’s that easy! Now you can reference your debt payoff plan at any time.

5. Put the Plan Into Action

At first glance, the spreadsheet may look overwhelming—especially compared to the simplified Debt Payoff Calculator. However, I find it incredibly motivating to see each month laid out. Plus, any extra payments we make beyond what’s on the sheet will further shorten our payoff timeline!

Now, it’s time to put the plan into action and start crushing this debt!

[featured image: Landscape Vectors by Vecteezy]

*This post may contains affiliate links, meaning I may earn a small commission if you subscribe. Most of the time, you’ll also get a bonus, so it’s a win-win!

I’d love to hear from you! How did you create your student loan repayment plan?

Leave a comment